Why Your Loan's Interest Rate and APR Are Not the Same

Lenders advertise a low interest rate, you sign the paperwork, and then the real cost of borrowing quietly shows up in your APR, which can be hundreds of dollars higher per year.

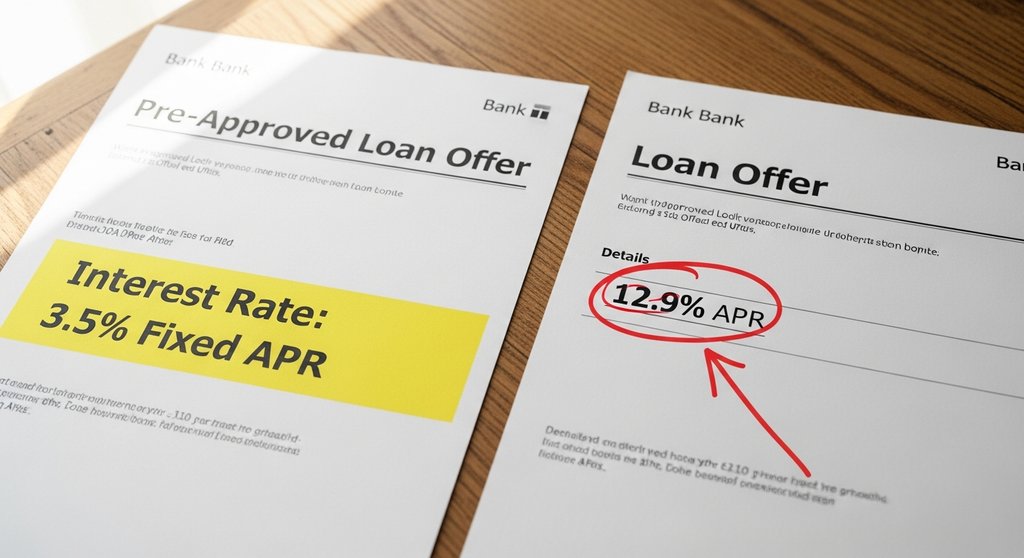

The Number Lenders Want You to Focus On

When a bank advertises a 6.5% personal loan, they mean the nominal interest rate, which is simply the percentage charged on the principal balance. That number looks clean and manageable. But it leaves out origination fees, closing costs, broker fees, and any other charge that comes with the loan.

The APR, or annual percentage rate, wraps all of those costs into a single annualized figure. On a $20,000 personal loan with a 2% origination fee, your stated rate might be 6.5% while your APR lands closer to 8.1%. Over a three-year term, that gap costs you roughly $340 extra in real money. Borrowers who shop by interest rate alone will consistently pick the wrong loan.

How Fees Transform a Competitive Rate Into an Expensive Loan

Consider two lenders competing for your auto loan business. Lender A offers 5.9% with no fees on a $30,000 loan over 60 months. Lender B offers 5.5% but charges a $600 origination fee. Lender B's lower rate sounds better, but after folding in that fee, its APR climbs to about 5.94%, making it the pricier option across the full repayment period. Try the loan APR calculator to see your own numbers.

This is exactly the kind of comparison that trips people up during rate shopping. The fee structure matters as much as the rate itself, and lenders are not always eager to surface that information upfront. Federal law requires disclosure of APR in lending agreements, but by the time you see it in fine print, you may already feel committed to the loan.

Using a loan APR calculator before signing anything lets you run both scenarios side by side in about 30 seconds. Plug in the principal, the rate, the loan term, and any fees, and the real annualized cost appears immediately. That number is what you should be comparing across lenders, not the headline rate.

Short Loan Terms Amplify the APR Effect

Loan term length changes how dramatically fees affect your APR. A $1,500 origination fee on a 30-year mortgage gets spread across 360 payments, nudging your APR only slightly above the stated rate. That same $1,500 fee on a 24-month personal loan hits much harder because it is compressed into far fewer payments, sending your APR noticeably higher.

This means short-term borrowers, including people using buy-now-pay-later plans, two-year personal loans, or payday-style installment products, face the sharpest distortion between advertised rate and true cost. A loan marketed at 9.99% with a flat $200 processing fee on a $3,000 12-month loan carries an APR of roughly 13.5%. That is a meaningful difference if you are trying to decide between paying with savings or borrowing.

One Calculation That Pays for Itself

The single best habit you can build before taking any loan is to calculate the true APR before agreeing to terms. Ask the lender for the full fee schedule, not just the rate sheet. Then run the numbers yourself rather than relying on the lender's summary.

A good loan APR calculator handles that calculation instantly and shows you the monthly payment, the total interest paid, and the effective annual cost all in one view. That gives you a complete picture rather than a single percentage that may hide half the story. With rates for personal loans still elevated compared to the pre-2022 environment, the spread between nominal rate and APR has become even more consequential for household budgets.