News & Articles

Finance basics, calculator guides, and personal finance explained.

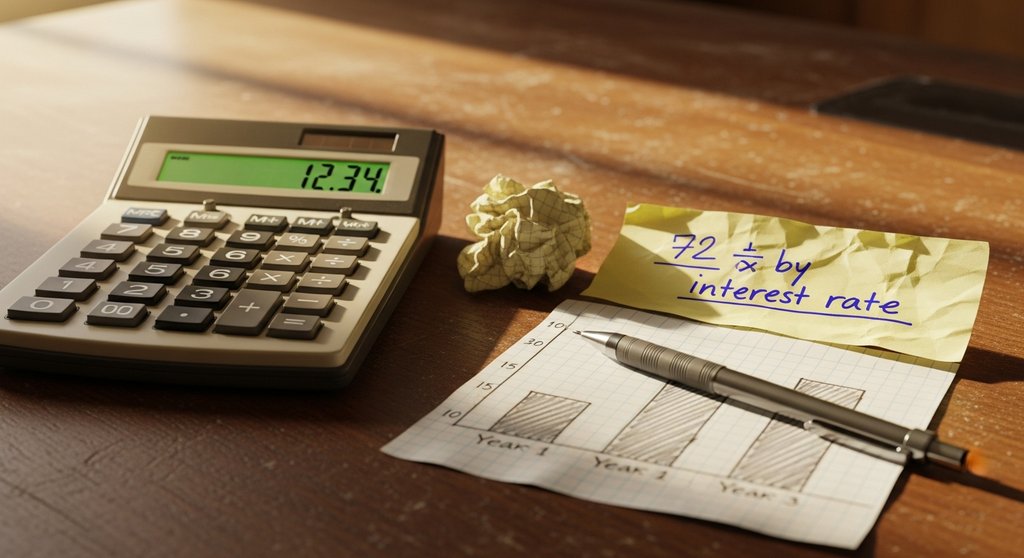

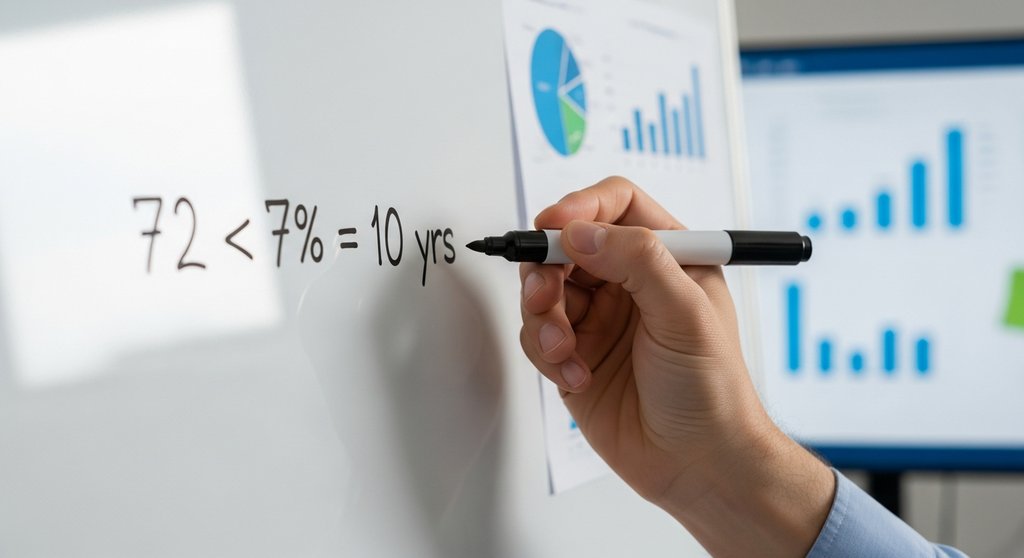

The Rule of 72 reveals how fast money doubles, but most investors misapply it. Learn the real math behind doubling time with concrete examples.

High mortgage rates have flipped the rent-vs-buy math in dozens of U.S. cities. See how long you really need to stay put before buying makes financial sense.

Most people guess their net worth wrong. Here's why liabilities change everything, and how to get an accurate number in under five minutes.

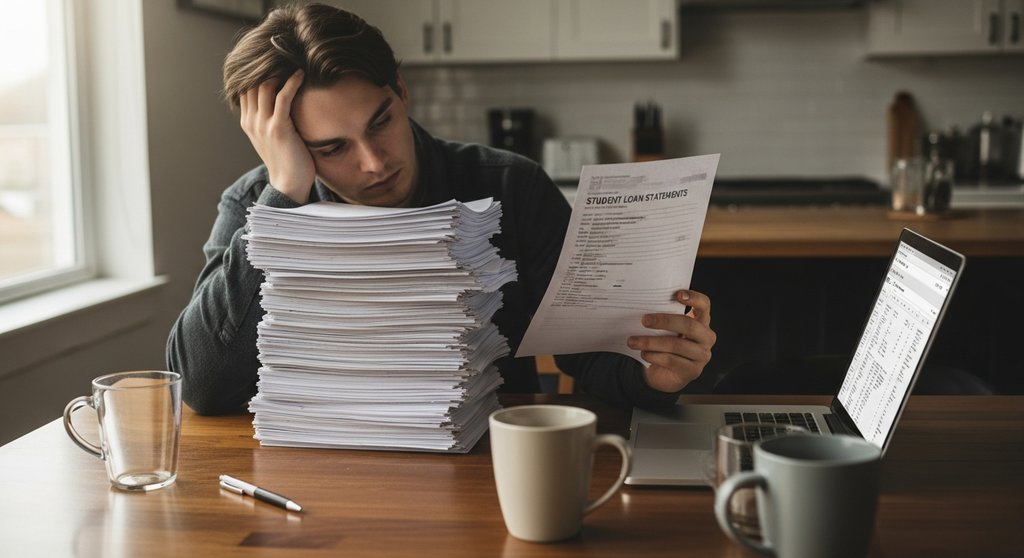

Making minimum student loan payments can leave you in debt for decades. Here's what the math actually looks like and how to fix it fast.

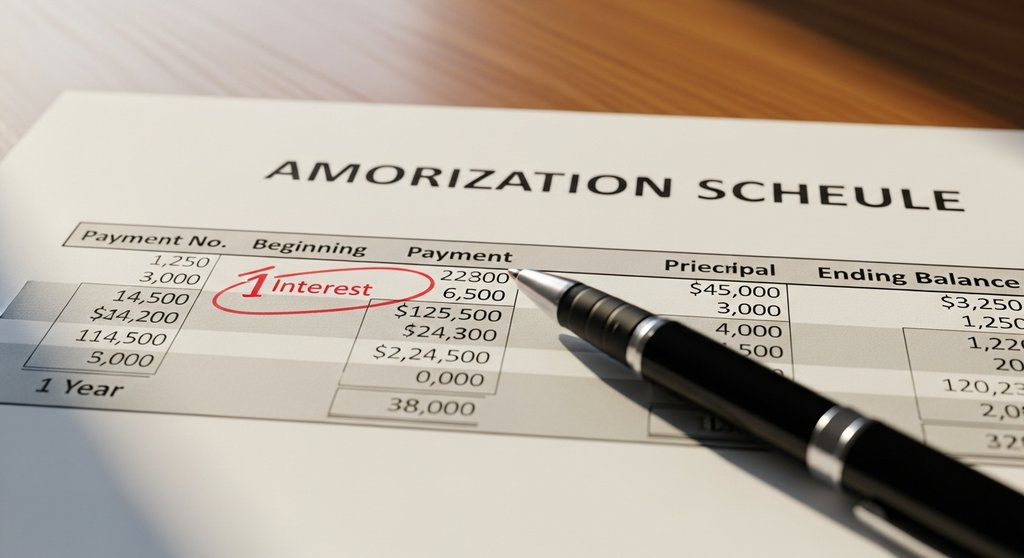

Most borrowers are shocked how little principal they pay early on. Here's why front-loaded interest is costing you more than you think, and how to fight back.

Most investors assume dollar cost averaging always wins. The data says otherwise. Here's when DCA actually makes sense and how to model it for your situation.

Holding an investment for 366 days instead of 365 can save you thousands in taxes. Here's how capital gains rates work and what most investors get wrong.

Lenders approve you for more than you can comfortably spend. Here's how to find your real home affordability number before you start shopping.

Most people underestimate their net worth by forgetting key assets. Here's what to include, what to skip, and why the number matters more than your salary.

A 20% discount and a 20% markup are not opposites. Learn why percent calculations trip people up and how to avoid costly math mistakes.

Most people tip on the wrong number without realizing it. Here's what the pre-tax vs. post-tax tipping debate actually costs you, with real examples.

Inflation quietly erodes real wages. See how much a 2010 salary is actually worth in 2024 and why most people underestimate cumulative price increases.

A 20% APR sounds manageable until you see the monthly math. Learn how daily compounding quietly inflates your credit card balance faster than expected.

Minimum payments feel manageable, but they cost you thousands in interest. See exactly how much with a debt payoff calculator before your next statement arrives.

Many investors underestimate their capital gains tax bill by forgetting holding periods. Here's what short-term vs long-term rates actually cost you.

Most people undercount assets or forget liabilities when estimating net worth. Here's how to get an accurate number and why it matters right now.

Adding just $50 to your monthly debt payment can save thousands in interest. Here's the math behind why small extra payments have such a big impact.

Most investors assume dollar cost averaging always wins. The math says otherwise. Here's what the research shows and when DCA actually makes sense.

Sales tax rates vary wildly by city, county, and state. Here's why your checkout total surprises you and how to calculate the real cost before you buy.

Dollar cost averaging feels safer than lump sum investing, but the math often disagrees. Here's what the data shows and when DCA genuinely wins.

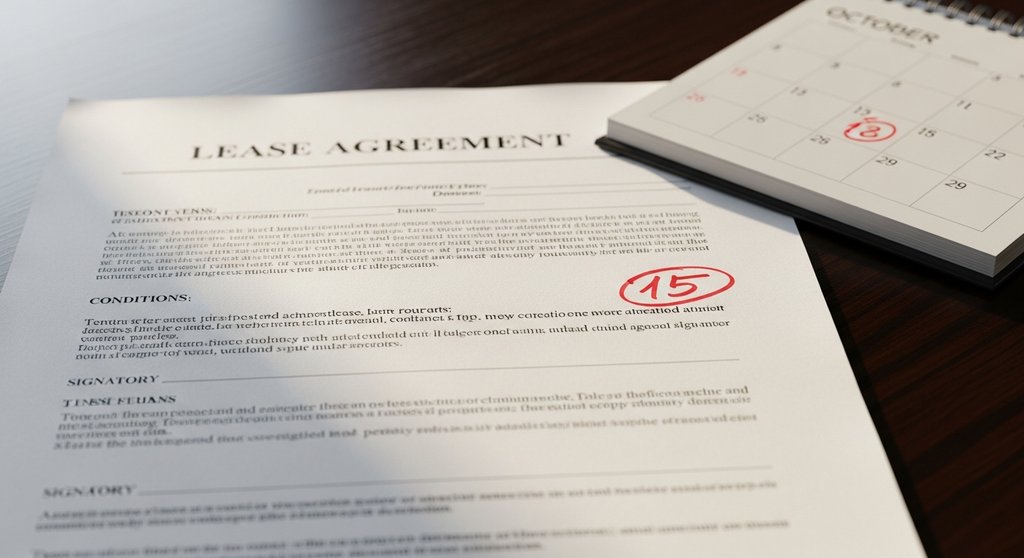

Miscounting days between dates is more common than you think. Learn why manual date math fails and how to get exact day counts fast for deadlines and contracts.

Most people underestimate how long saving $10,000 takes. See how contribution size and interest rate change your timeline dramatically.

A $60,000 salary in 2015 buys far less today. Learn how inflation erodes real income and why adjusting for purchasing power changes every financial decision.

Sales tax rates vary wildly by city and product type. Learn why your checkout total always surprises you and how to budget accurately before you buy.

A high credit score won't save a mortgage application if your debt-to-income ratio is too high. Here's what lenders actually check first.

The Rule of 72 is a handy shortcut, but it breaks down at extreme interest rates. Learn when to trust it and when to double-check your math.

Most people misread how credit card APR actually works. Here's what daily periodic rates really cost you, with concrete numbers and a calculator to check your own card.

Confusing markup and margin is one of the most common small-business pricing errors. Learn the difference and how to price products for real profit.

A 24% APR sounds manageable until you do the math. See how daily compounding quietly inflates your credit card balance month after month.

Millions of Americans guess their retirement savings target and guess wrong. Here's the math behind a realistic number and how to calculate yours today.

Miscounting days between dates costs renters and landlords money. Learn how to calculate date differences accurately and avoid expensive lease mistakes.

Most small business owners forget variable costs when finding their break-even point. Here's the mistake that kills margins and how to fix it fast.

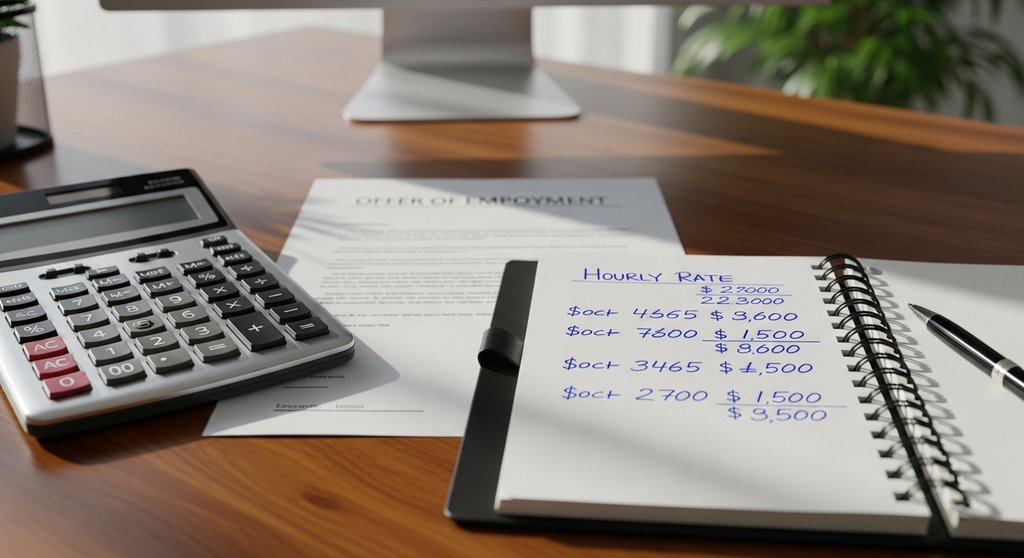

Most people miscalculate their real hourly rate by ignoring unpaid time off and benefits. Here's what your salary actually works out to per hour.

Many small business owners underestimate their true break-even point by forgetting semi-fixed costs. Here's how to get the number right from the start.

Most small business owners overestimate their break-even point by ignoring variable cost ratios. Here's how to calculate it correctly and price smarter.

Most savings accounts are losing ground to inflation right now. Learn how to calculate your money's real purchasing power and what to do about it.

Most people misread how credit card APR works daily. Learn how daily periodic rates quietly inflate your balance and what that really costs you each month.

Inflation has quietly eroded purchasing power since 2019. Find out how much a dollar from five years ago is really worth today, with real numbers.

Lenders approve the maximum you can borrow, not what you can comfortably afford. Here's how to find your real home-buying budget before you start shopping.

A $60,000 salary isn't $28.85 an hour once you subtract unpaid overtime and lunch breaks. Here's what your pay really looks like hourly.

The 50/30/20 budget rule sounds simple, but middle-income earners often find it quietly failing them. Here's why, and how to fix it fast.

Most borrowers are shocked to see how little principal they pay in the early months. Here's why amortization front-loads interest and what it costs you.

A $60,000 salary sounds solid, but your real hourly rate might shock you. Here's how to calculate what you actually earn per hour worked.

Most people underestimate how long saving takes. A savings goal calculator reveals the real timeline, and what small changes actually move the needle.

The old '3-month emergency fund' rule may leave you dangerously short. Here's what the math actually says about how much cash cushion you need right now.

High interest rates make future payments worth far less today. Learn how present value math exposes the real cost of deferred settlements and payment plans.

Most borrowers focus on credit scores, but your debt-to-income ratio is what actually blocks mortgage approvals. Here's what lenders see and how to fix it.

The 'renting is wasting money' myth costs people thousands. See the real numbers behind renting vs. buying in a high-rate environment.

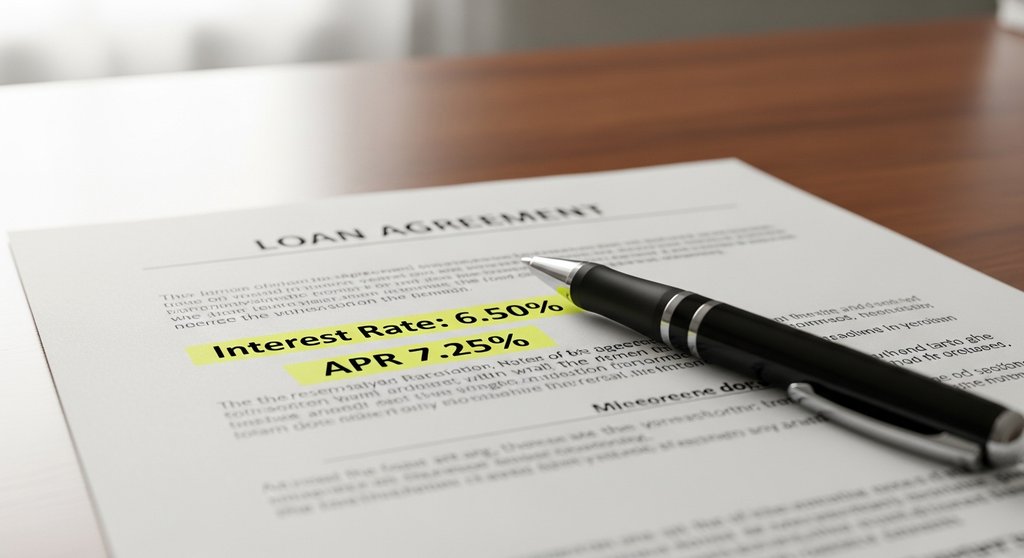

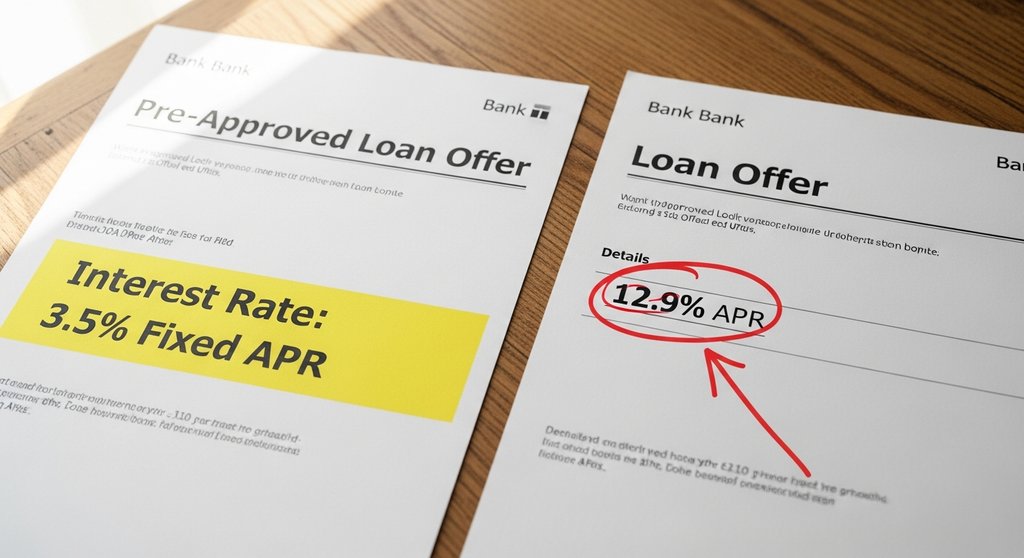

Borrowers often confuse interest rate with APR and end up shocked by the true cost of a loan. Here's what the difference actually means for your wallet.

Many small business owners undercount fixed costs and set prices too low. Here's how to find your real break-even point before you lose money.

High mortgage rates changed the rent vs buy math. See which option saves more money in your city before you sign anything in 2025.

A low monthly car payment can hide a brutal total cost. Learn how loan term length quietly inflates what you pay and how to spot the trap before you sign.

The 50/30/20 budget rule sounds simple, but middle-income earners often find rent alone blows the 50% needs cap. Here's how to fix it.

Many borrowers confuse interest rate with APR and end up paying more than expected. Here's what the difference actually costs you in real dollars.

A low interest rate can hide a brutal monthly payment. Here's what most buyers miss when comparing mortgage offers in 2025.

Lenders often care more about your debt-to-income ratio than your credit score. Here's what a good DTI looks like and how to fix a bad one fast.

Most people overestimate future payments. Learn how present value math reveals what that lump sum, pension, or settlement is actually worth right now.

Most people guess at a monthly savings number and hope for the end result. Here's how to work backward from your goal and actually get there on time.

Paying the minimum on student loans but watching the balance crawl down? Here's why interest front-loading traps borrowers and how to fix it fast.

BMI is widely used but widely misunderstood. Learn when your body mass index number is a useful health signal and when it genuinely misleads you.

Most people tip on the wrong number without knowing it. Here's what the pre-tax vs post-tax tipping debate actually costs you, with real examples.

A 24% APR sounds straightforward, but daily compounding makes the real cost much higher. Here's what your credit card bill isn't telling you.

A sky-high dividend yield can signal a bargain or a value trap. Learn how to read yield figures correctly before chasing income in any rate environment.

Retailers use percentage tricks that make discounts look bigger than they are. Learn how to check the real math before you spend a cent.

The classic '3-month rule' for emergency funds leaves millions exposed. Here's why your real number is likely higher and how to calculate it fast.

Think your pay raise beat inflation? Most people overestimate their real wage growth. Here's how to check what your old salary is actually worth today.

The '3-month rule' for emergency funds is outdated for many households. Here's how to calculate exactly what you need based on your real risk profile.

Most people underestimate how long saving takes. See how deposit size and interest rate affect your timeline using a savings goal calculator.

Most investors assume dollar cost averaging is always safer than lump sum investing. The data tells a more complicated story. Here's what you need to know.

Most people only use the Rule of 72 for investments, but it's just as powerful for tracking debt growth. Here's how to use it smarter in a high-rate environment.

Sales tax rates vary wildly by city and product type. Learn why checkout totals surprise shoppers and how to calculate the exact amount before you buy.

Most Americans tip on the post-tax bill without thinking twice. Here's why tipping on the pre-tax subtotal saves real money and how to do it quickly.

The Rule of 72 is a quick mental math shortcut, but most investors misapply it. Here's how to use it correctly and when it actually breaks down.

Borrowers often confuse interest rate with APR and end up paying more than expected. Here's what the difference actually costs you in real dollars.

Most borrowers are shocked how little principal they repay early on. Here's the math behind front-loaded interest and how to use it to your advantage.

The 50/30/20 budget rule sounds simple, but it quietly fails many middle-income earners. Here's where the math goes wrong and how to fix it.

The '3-month rule' for emergency funds is outdated for many households. Here's how to calculate the right cushion for your actual situation.

Inflation erodes purchasing power silently. Find out what a salary or price from any past year is actually worth in today's dollars, with real numbers.

The 'renting is wasting money' myth costs homebuyers thousands. See what the real numbers say before your next housing decision.

Most people tip on the wrong number without realizing it. Here's what etiquette experts and servers actually say about the pre-tax vs post-tax tip debate.

Many new business owners forget variable costs when calculating break even. Here's how to find your real number before you run out of cash.

Many borrowers confuse interest rate with APR and end up paying more than expected. Here's what the difference actually costs you in real dollars.

Most borrowers are shocked how little principal they pay early on. Here's why front-loaded interest works against you and what to do about it.

The '3-month rule' for emergency funds is outdated for millions of households. Here's how to calculate exactly what you need based on your real risk profile.

Banks advertise APR, but your balance grows by APY. Here's why the gap matters and how to calculate your real annual earnings in under a minute.

Most people tip on the wrong number without realizing it. Here's what etiquette experts say and how to calculate the right tip every time.

Got a raise over the past decade but feel no richer? Inflation erosion explains why. See how to calculate your salary's real purchasing power loss.

Many borrowers confuse interest rate with APR and end up paying more than expected. Here's what the difference actually means for your monthly budget.

A 24% APR sounds like a yearly rate, but credit cards charge interest daily. See exactly how much that misconception costs you each month.

A high dividend yield sounds like free money, but it often signals trouble. Learn what the number really means before you buy income stocks.

A $60,000 salary in 2015 buys much less today. Learn how cumulative inflation quietly erodes real income and how to calculate the true difference.

Rising interest rates quietly shrink your net worth even when your income stays the same. Here's what changed and how to recalculate accurately.

A low monthly car payment often hides a much higher total cost. Here's how to spot the real price of your auto loan before you sign anything.

Mixing up markup and margin is a common pricing mistake that silently shrinks profits. Here's how to tell them apart and price your products correctly.

The 'save 10% and you're fine' rule is dangerously outdated. Here's what modern retirement math actually looks like and how to fix your number fast.

Sales tax, fees, and stacked discounts distort what you actually save. Here's how percentage math tricks shoppers and how to check your receipts fast.

Lenders approve you for the max you can borrow, not what you can comfortably spend. Here's how to find your real home affordability number.

Borrowers often confuse interest rate with APR, and that confusion can cost hundreds. Here's what APR actually includes and how to compare loans fairly.

A $60,000 salary in 2015 buys far less today than it did then. Here's how to use inflation-adjusted value to see what your money really lost.

Low monthly payments on car loans often hide sky-high total interest costs. Here's how to spot the real price of financing your next vehicle.

BMI can flag you as overweight even when you're healthy. Here's what the number actually measures, where it fails, and how to read it correctly.

High mortgage rates have flipped the rent vs buy math in dozens of U.S. cities. Here's how to run the real numbers before you commit to a 30-year loan.

Banks advertise APR, but your money grows at APY. Learn why these two rates differ and how compounding frequency quietly changes your real return.

Most people tip on the wrong number without knowing it. Here's the pre-tax vs post-tax tipping debate settled with real math and a free tip calculator.

Paying just $50 extra toward credit card debt each month can save hundreds in interest. Here's the math most people miss and how to use it.

A 24% APR sounds annual, but credit cards charge interest daily. See exactly how much that misconception costs you each month with real numbers.

A mortgage pre-approval tells you what a lender will give you, not what you should spend. Here's how to find your real home affordability number.

CD rates hit multi-decade highs and many savers are still sitting in 0.5% savings accounts. Here's how to calculate what you're actually leaving on the table.

BMI is widely used but frequently misunderstood. Learn when the number is genuinely useful, when it misleads, and how to read your result with context.

Lenders use your debt-to-income ratio as a hard cutoff, not just a guideline. Learn why 43% matters and how to check yours before applying.

Most people assume DCA always wins. The data tells a different story. Here's when dollar cost averaging helps and when it quietly costs you returns.

Most borrowers are shocked how little principal they pay in early months. Here's why amortization front-loads interest and what to do about it.

Lenders care about your debt-to-income ratio almost as much as your credit score. Learn what DTI threshold gets you approved and how to calculate it fast.

A home renovation can trigger a reassessment that spikes your property tax bill. Here's how to estimate the hit before you swing the first hammer.

Most people tip on the wrong number without realizing it. Here's what the pre-tax vs. post-tax tipping debate actually means for your wallet and your server.

Many investors don't realize holding a stock one extra day can slash their tax bill. Here's how short vs long-term capital gains rates actually work.

Most people guess their retirement savings target too low. Here's the math behind why, and how to calculate a realistic number before it's too late.

Lenders approve you for the maximum they'll lend, not the maximum you should spend. Here's how to find your real home affordability number.

Many borrowers confuse interest rate with APR and end up paying more than expected. Here's what the gap actually means for your next loan.

BMI is useful but widely misunderstood. Learn what your number actually means, where it fails, and how to use it alongside other health markers.

Your credit card APR isn't charged once a year. Learn how daily compounding quietly inflates what you owe and how to calculate the real cost fast.

The Rule of 72 is a handy shortcut for doubling time, but most people apply it wrong. Here's what it actually tells you and when to trust it.

Millions of borrowers confuse interest rate with APR and end up surprised at closing. Here's what the difference actually costs you in real dollars.

Banks approve you for more than you can comfortably afford. Here's how to find your real monthly mortgage limit before you fall in love with a house.

Millions underestimate how much they need to retire comfortably. Here's the math behind the shortfall and how to fix your projection now.

Many entrepreneurs get their break-even math wrong by ignoring semi-fixed costs. Here's how to find the real number before you open the doors.

Many borrowers are surprised by their actual monthly student loan bill. Here's what's really driving the number and how to calculate it accurately.

CD rates have shifted heading into mid-2026. Here's how to calculate your real return before you commit to a term, including the tax bite you might be missing.

The Rule of 72 reveals how long your money takes to double. With rates shifting in 2026, here's why this shortcut is more useful than ever.

A low monthly car payment sounds great, but it can cost thousands extra in interest. Here's what to check before you sign anything at the dealership.

Your lender's mortgage quote rarely matches your actual monthly payment. Here is what gets left out and how to calculate the real number before you sign.

The 50/30/20 budget rule works at modest incomes but breaks for high earners. See why needs shrink as income rises, with a $40k vs $150k example.

Most people guess their net worth from their bank balance and get it wrong. Here is how to count every asset and liability and find your real number.

The claim that renting throws money away ignores owners' non-equity costs and the opportunity cost of a down payment. Here is the honest rent vs buy math.

APY includes compounding and APR does not. Learn why a savings APY beats the stated rate and why a loan APR understates cost, with a worked example.

Most owners miscalculate break-even by ignoring variable costs. Learn the contribution margin formula with a worked small-business break-even example.

Tipping on the pre-tax or post-tax total changes your bill by only cents to a couple dollars. See US tipping norms and a worked example on an $80 check.

Holding an investment one year and a day instead of less can cut your capital gains tax in half. Here is how short-term and long-term rates really work.

A dollar in five years is worth less than a dollar today. Here is how present value and the discount rate work, with a worked example on $1,000 in the future.

Your savings goal feels stuck because monthly contributions, interest, and time interact in ways most plans ignore. See a worked $20,000 savings example.

Dollar cost averaging in a rising market often trails lump-sum investing, but it still protects against bad timing. Here is what DCA really buys you.

A great credit score can still get a mortgage denied. Here is how lenders use your debt-to-income ratio, the 43% threshold, and front-end vs back-end DTI.

A static emergency fund quietly loses buying power every year. Here is how inflation erodes your cash cushion and how to top it up and where to hold it.

Paying only the minimum or stretching to an extended term can double what a student loan costs. Here is how interest piles up and how extra principal helps.

A 401k employer match is free money, but front-loading contributions or under-saving can forfeit it. Here is how match formulas work and how to keep it.

The student loan grace period is six months, but interest can accrue and capitalize during it. Here is what that does to your first payment and balance.

Markup and margin use the same dollars but different bases, so a 50% markup is only a 33% margin. Here is how to tell them apart and price correctly.

A mortgage pre-approval is the most a lender will give you, not what you can comfortably afford. Here is the gap between the ceiling and a real budget.

Most people guess their student loan payment too low because they ignore amortization. Here is how the standard 10-year payment is really calculated.

BMI is a quick screening tool, not a verdict. Learn the formula, where BMI misleads for athletes and older adults, and what to check alongside the number.

Size your emergency fund by essential monthly expenses, not income. See when the 3-month rule falls short and a worked example for sizing your safety net.

A percent calculator helps avoid the everyday errors people make with tips, sales tax, and discounts. Here are the mistakes and how to get the math right.

Your true hourly rate is lower than the salary-to-hourly math suggests once you count unpaid overtime, commuting, and job costs. Here is how to find it.

A high dividend yield can flag a falling stock price or an unsustainable payout. Learn the yield formula, the payout ratio test, and how to spot a yield trap.

Interest rate vs APR explained: APR folds in fees, so it runs higher. Learn why, how to compare loans fairly, and a worked example with origination fees.

Learn how compound interest works, see a real $1,000 example, and discover why starting early makes such a big difference.

Lottery, pension, and settlement offers force a lump sum vs annuity choice. See how the discount rate and present value decide which deal is actually larger.

A rent vs buy breakdown using the price-to-rent ratio and breakeven math. See the hidden costs of owning and the cities where renting still wins in 2026.

The Rule of 72 estimates how long money takes to double. See where the shortcut stays accurate, where it drifts, and worked examples at 6%, 9%, and 12%.

A 2015 salary buys less today thanks to cumulative inflation. Learn the difference between nominal and real pay and how to compare wages across the years.

The car loan total you pay can far exceed the sticker price. See how term length and interest rate quietly inflate what that vehicle really costs you.

Small extra principal payments cut total interest and shorten payoff time fast. See a worked example of how an extra $100 a month transforms a loan.

Your credit card APR understates what a balance really costs. Learn how the daily periodic rate and compounding push the effective cost past the stated APR.

Rising home values and millage rates both shape your property tax bill. Learn how assessments, caps, and appeals decide what you actually owe each year.

Converting an annual salary to a true hourly rate reveals what you really earn. Here is how unpaid extra hours quietly shrink your real pay per hour.

Counting the exact days between two dates sounds simple, but lease deadlines and notice periods trip people up. Here is how to count days correctly every time.