Why Your Loan's Interest Rate and APR Are Not the Same Thing

Millions of borrowers sign loan agreements every year thinking the interest rate is the number that matters most, but the APR is usually the one that tells the real story.

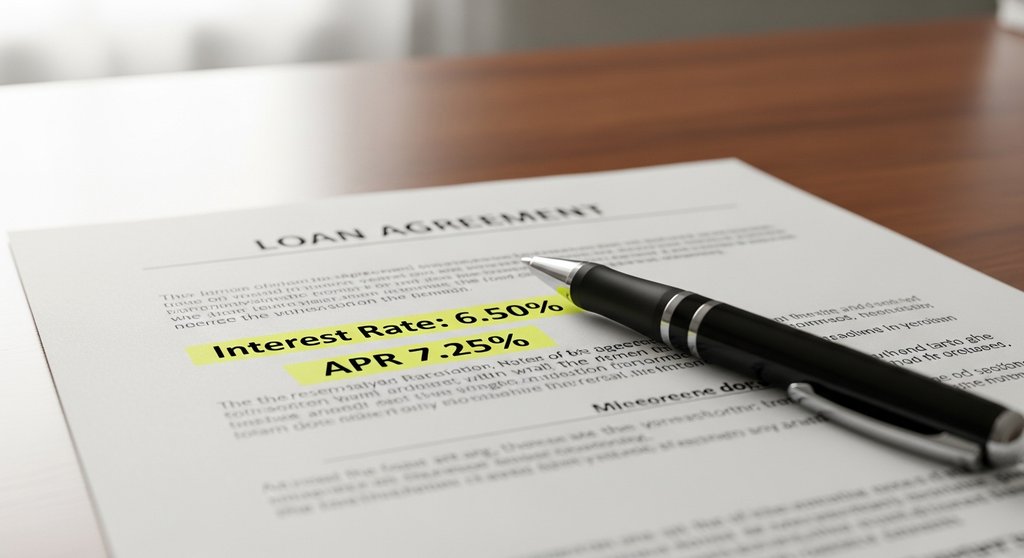

The gap between 6.5% and 8.2% is not a rounding error

A lender quotes you a 6.5% interest rate on a $25,000 personal loan. Sounds reasonable. But buried in the fine print is an origination fee of 4%, plus a monthly account maintenance charge. When those costs get folded into the Annual Percentage Rate, the APR jumps to 8.2%. On a 48-month term, that difference adds up to roughly $950 in extra costs you never saw coming.

The interest rate only captures what the lender charges you on the outstanding principal. The APR captures the interest rate plus almost every fee rolled into the cost of borrowing. Federal law under the Truth in Lending Act requires lenders to disclose the APR, specifically because the interest rate alone is too easy to misrepresent.

What actually gets included in the APR calculation

Origination fees, underwriting fees, mortgage broker fees, and certain closing costs all feed into the APR. For mortgages specifically, private mortgage insurance (PMI) and prepaid interest can also factor in depending on the lender and loan type. The result is a single percentage that lets you compare two loans on an apples-to-apples basis, even when their fee structures look completely different. Try the loan APR calculator to see your own numbers.

What the APR does not include: late payment penalties, prepayment penalties, and optional add-ons like credit life insurance. So the APR is a floor, not a ceiling. If you pay late or pay off early on a loan with a prepayment clause, your true cost of borrowing climbs even higher than the APR suggests.

This is why comparing only the interest rates across three loan offers is a classic mistake. Lender A at 7.0% with minimal fees may be genuinely cheaper than Lender B at 6.75% with a 3% origination charge, once you run the actual APR math.

Short loan terms make the APR diverge even faster

Here is something most borrowers miss: fees hit harder on short-term loans. A $500 origination fee on a 5-year loan spreads its damage across 60 months. The same fee on a 12-month loan compresses entirely into one year, pushing the APR up sharply. This is why payday loans and short-term personal loans often carry APRs in the triple digits even when the flat fee seems modest.

Take a $1,000 two-week payday loan with a $75 fee. The interest rate stated might be 7.5% for the two-week period, which sounds harmless. Annualized as an APR, that same loan costs 195%. The math is not wrong; it is just showing you what it would cost if you rolled that loan over for a full year. Knowing this helps you decide whether a quick cash advance is actually your cheapest option.

Running the numbers before you sign anything

Before accepting any loan offer, plug the principal, interest rate, loan term, and all known fees into a loan APR calculator to see the true annualized cost. Most people do this comparison only after they are already sitting across from a loan officer, which is too late to negotiate effectively. Doing it the night before gives you real leverage.

If two lenders are within 0.25% of each other on APR, the decision probably comes down to customer service and flexibility. But if one APR is a full percentage point higher, that gap matters: on a $30,000 auto loan over five years, one point of APR costs you approximately $790 extra in total payments. That is not abstract math; it is real money you could keep.